What if the most critical design choice for your Buffalo enterprise isn't the layout of your studio, but the invisible framework of your tax status? For many Western New York founders, the choice between an s corp vs llc new york tax structure is the difference between a foundation that breathes and one that feels restrictive. You likely feel the weight of the 15.3 percent self employment tax. It's a structural leak that can stall the momentum of even the most intentional business.

We agree that the complexity of the New York State Department of Taxation shouldn't stifle your professional vision. This guide reveals the material tax differences between these structures, offering you a clear roadmap for compliance and structural integrity. You'll learn to identify the $60,000 profit threshold where an S-Corp election often becomes the more efficient choice for your bottom line. We'll examine the specific requirements for filing in Albany and how to align your business entity with your long term financial goals.

Key Takeaways

- Understand the structural distinction between an LLC’s operational flexibility and the S-Corp as a deliberate tax election designed for fiscal efficiency.

- Navigate the s corp vs llc new york tax landscape to identify how specific pass-through structures impact your personal returns and self-employment obligations.

- Evaluate the tectonic shift in administrative craft and compliance fees required to maintain a more complex corporate framework within New York State.

- Pinpoint the specific "break-even" profit threshold where transitioning to an S-Corp becomes a sound design choice for your Buffalo-based enterprise.

- Learn how to integrate entity evolution with proactive tax planning to ensure your financial foundation remains resilient and site-specific.

The Foundation of Formation: Navigating New York Entity Landscapes

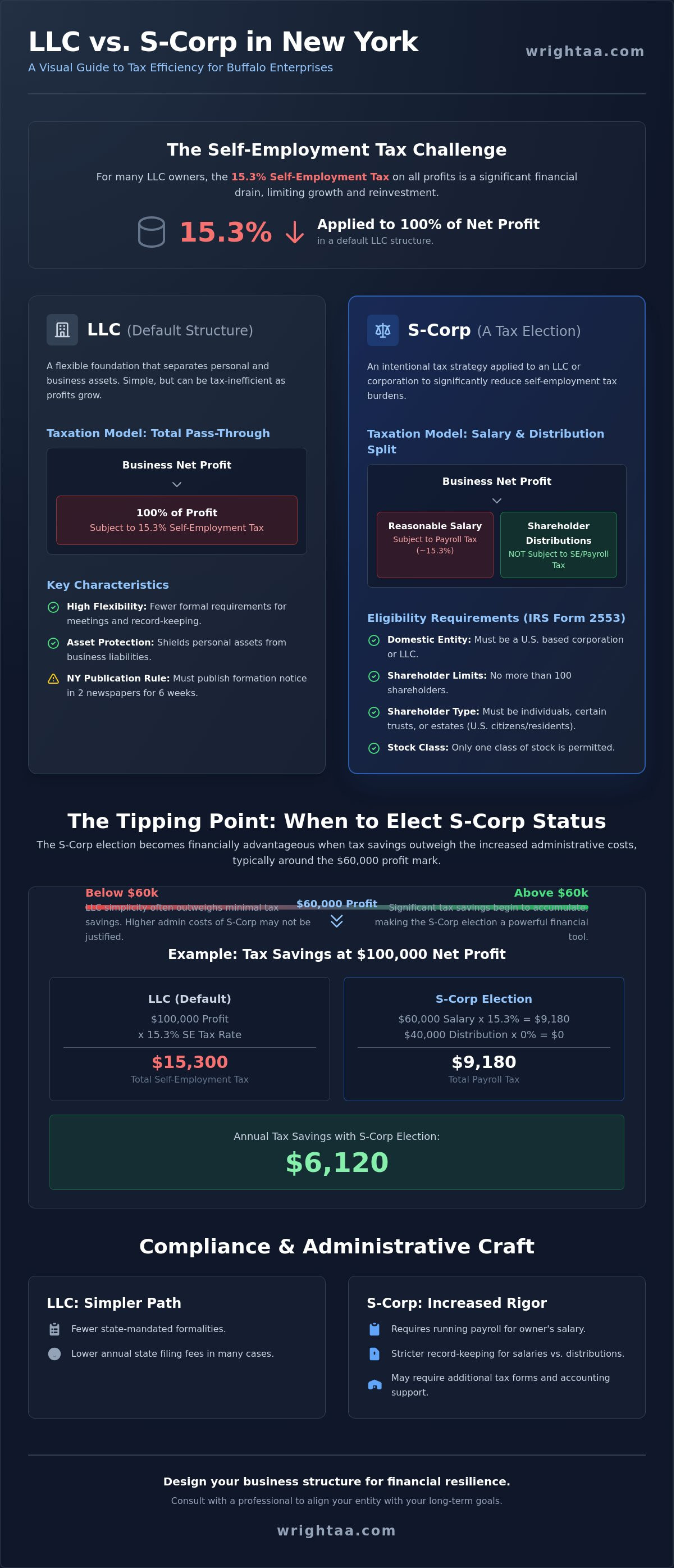

In the architectural landscape of Western New York, a structure is only as resilient as its base. For entrepreneurs in Buffalo and Rochester, the initial choice between an s corp vs llc new york tax designation represents more than a legal formality; it is a deliberate act of design. The Limited Liability Company (LLC) serves as the flexible vernacular of the modern business, offering a site-specific solution that adapts to the shifting needs of a startup. Many founders mistakenly view the S-Corp as a separate physical entity. It is, in reality, a refined tax election layered onto an existing structure.

The New York Department of State oversees the tectonic shifts of business formation across the state. While the department provides the framework for filing, it does not dictate the financial efficiency of the result. Selecting a "default" classification often leads to a misalignment between a company’s growth and its tax obligations. A thoughtful maker understands that the foundation must support not just the current weight of the enterprise, but its future elevation.

The LLC: A Versatile Starting Point

For a single-member LLC in Western New York, simplicity is the primary material. This structure creates a necessary boundary between personal assets and business risks, much like a well-insulated envelope protects an interior from the Buffalo winter. It allows for pass-through taxation, where profits flow directly to the owner without the complexity of corporate layers.

New York imposes a unique requirement that demands an initial investment of time and capital. Under Section 206 of the Limited Liability Company Law, new entities must publish a notice of formation in two newspapers for six consecutive weeks. This process must be completed within 120 days of filing. While this adds a layer of administrative craft to the process, it remains a vital step in establishing a legitimate presence within the state’s regulatory environment.

The S-Corp: Elevating Your Tax Classification

Shifting to an S corporation federal tax status represents a transition from a default state to an intentional tax strategy. This election, made via IRS Form 2553, allows the business to be treated as a partnership for tax purposes while maintaining the corporate veil. It is a dialogue between federal and state recognitions that requires precise timing and eligibility.

To qualify for this status in 2026, the IRS maintains strict requirements:

- The entity must be a domestic corporation or LLC.

- It may have no more than 100 shareholders.

- Only one class of stock is permitted to maintain structural clarity.

- Shareholders must be U.S. citizens or residents.

The Tectonics of Taxation: Pass-Through Entities in Buffalo

Structure dictates flow. In the geography of business, pass-through taxation acts as a transparent conduit, where the profit of the enterprise moves directly to the owner's personal tax return. This connection is immediate and absolute. For a Buffalo entrepreneur, the business itself doesn't pay federal income tax; instead, the owner absorbs the tax responsibility at their individual rate. While this avoids the "double taxation" of a traditional corporation, it exposes every dollar of profit to the owner's personal tax bracket.

The weight of this structure becomes apparent when we examine the 15.3% Self-Employment (SE) Tax. In a default LLC, the IRS views the owner and the business as a single entity for tax purposes. This means the entirety of your net income is subject to Social Security and Medicare levies. When you layer this on top of the projected New York State personal income tax rates for 2026, which range from 4% to 10.9% for high earners, the cumulative burden is substantial. Many Buffalo business owners overpay because they remain in a default LLC structure long after their profit margins have scaled beyond the need for such simplicity. They're essentially paying a premium for a lack of structural nuance.

Self-Employment Tax vs. Payroll Tax

The IRS maintains a distinct boundary between an owner's labor and their investment. In an LLC, this distinction is blurred, as all "draws" are treated as earned income. The S-Corp structure introduces a deliberate separation. It requires the owner to receive a W-2 salary, while the remaining profit is distributed as a dividend. The self-employment tax rate of 15.3% serves as a primary pain point for growing firms because it applies to the entire net income in an LLC.

By implementing an S-Corp strategy, you only pay that 15.3% on the salary portion. The cornerstone of this approach is "Reasonable Compensation." This is a defensible, market-based salary that reflects the actual value of your work. Any profit exceeding this salary is exempt from the 15.3% SE tax, allowing for significant capital preservation that can be reinvested into the craft of your business. This is the essence of thoughtful financial design.

New York State Specific Tax Nuances

New York’s tax landscape requires a site-specific approach. The state recognizes the S-Corp election, but it treats the components of income differently. While wages are subject to standard withholding, distributions are often treated more favorably at the state level. A vital development for Buffalo firms is the New York State Pass-Through Entity Tax (PTET). This elective tax allows S-Corps and partnerships to pay state income tax at the entity level.

- SALT Cap Relief: The PTET acts as a workaround for the $10,000 federal cap on state and local tax deductions.

- Direct Credits: Owners receive a corresponding credit on their NYS personal returns, effectively turning a personal expense into a business deduction.

- Buffalo Context: For businesses in the City of Buffalo, integrating PTET strategies helps mitigate the combined pressure of state and local economic realities.

Understanding the s corp vs llc new york tax distinction is about more than just numbers; it's about aligning your business's legal form with its economic reality. When the foundation is designed with precision, the entire structure stands more resilient against the shifts in the tax code.

Material Differences: NY State Compliance and Administrative Burdens

The structural integrity of a business depends on the quality of its maintenance. Just as a building requires a specific cadence of care to preserve its materiality, a business entity demands a disciplined approach to compliance. When evaluating the s corp vs llc new york tax landscape, the administrative burden represents a significant part of the total cost of ownership. It's the difference between a self-sustaining landscape and one that requires constant, meticulous pruning. This section examines the tectonic requirements of New York state law and how they impact your daily operations.

The New York S-Corp Election (Form CT-6)

A common misconception in the Buffalo business community is that a federal S-Corp election automatically applies to state obligations. New York requires its own specific gesture of intent. To achieve recognition in Albany, you must file Form CT-6. This filing must occur within two months and 15 days of the start of the tax year. If you miss this March 15 deadline for a calendar year business, the state will treat your entity as a C-Corp. This creates a mismatched tax profile. You may find yourself paying a corporate-level tax to the state while maintaining a pass-through status with the IRS. This lack of alignment often results in expensive remedial filings and lost tax efficiency.

LLC Maintenance and the Publication Requirement

The New York LLC offers a more fluid internal structure, yet it carries a unique local burden known as the publication requirement. Under Section 206 of the Limited Liability Company Law, new entities must publish a notice in two newspapers for six consecutive weeks. In Erie, Monroe, and Onondaga counties, this process is a necessary rite of passage. The cost for this administrative task typically ranges from $300 to $1,000 depending on the specific county and newspaper rates. Failure to complete this within 120 days of formation can lead to a suspension of your authority to do business.

Ongoing maintenance for an LLC involves the annual filing fee, submitted via Form IT-204-LL. This fee is a sliding scale based on the previous year's New York source income. For example, an LLC with income between $250,000 and $500,000 pays a flat fee of $500. Unlike the S-Corp, which requires formal corporate minutes and a rigid payroll schedule for owners, the LLC operates through a simpler Operating Agreement. This document serves as a living foundation, allowing for spatial breathing room in how you manage internal affairs.

- S-Corp Rigor: Requires quarterly payroll filings and annual corporate minutes to maintain the liability shield.

- LLC Simplicity: Offers a streamlined management style but requires the initial publication "tax" and annual filing fees.

- Soft Costs: The time spent on S-Corp payroll administration often outweighs the hard cost of LLC filing fees for smaller operations.

The choice between an s corp vs llc new york tax strategy often rests on your tolerance for these recurring tasks. An S-Corp requires a rigorous commitment to the craft of bookkeeping. The LLC offers a more vernacular approach, favoring simplicity over complex corporate formalities. Balancing these soft costs of time with the hard costs of tax payments is essential for a sustainable foundation.

Designing Your Choice: When Buffalo Businesses Should Elect S-Corp Status

Every structure reaches a point where its internal support must evolve to handle a greater load. In the context of the s corp vs llc new york tax debate, this tipping point is defined by net profit. For Buffalo entrepreneurs, the transition from a standard LLC to an S-Corp election is a deliberate act of financial engineering. It's a shift from a simple, fluid entity to one with a more rigid, yet efficient, internal framework.

The decision to elect S-Corp status usually gains clarity when a business's net profit reaches the $60,000 to $75,000 range. At this level, the tax savings begin to outweigh the administrative costs of maintaining payroll and increased filing requirements. In 2022, a Rochester law firm reached $110,000 in net income and decided to make this structural shift. By setting a reasonable salary and taking the remaining profit as a distribution, they realized a tax reduction of approximately $6,200 in their first year alone. This transition requires a steady monthly rhythm, as payroll services must be integrated into your financial life with the same precision as a site-specific architectural plan.

The S-Corp Savings Blueprint

The primary advantage of the S-Corp is its ability to bisect income. By paying yourself a "reasonable salary," you only pay the 15.3% self-employment tax on that specific portion of your earnings. The remaining profit flows through as a distribution, untouched by Social Security or Medicare taxes. S-Corp status can save a business $5,000+ annually if profit exceeds salary needs. This structural choice also interacts with the Section 199A deduction. While the 20% Qualified Business Income (QBI) deduction applies to both entities, the S-Corp's W-2 wages can sometimes provide a more stable foundation for this deduction in high-earning scenarios.

When the LLC Remains the Superior Design

There are times when the simplicity of the LLC is the more elegant solution. The LLC offers a spatial flexibility that the S-Corp lacks, particularly regarding ownership limits and membership types. If your business holds real estate, the S-Corp is often a poor choice. Placing property inside an S-Corp can lead to significant tax complications upon distribution or sale, as the IRS treats these events with less leniency than it does within an LLC framework.

- Passive Income: Rental income and dividends are already exempt from self-employment tax, rendering the S-Corp's primary benefit redundant.

- Administrative Weight: If your profit is below $50,000, the cost of corporate tax returns and payroll processing creates unnecessary friction.

- Ownership Diversity: LLCs allow for varied classes of membership, while S-Corps are restricted to a single class of stock and a 100-shareholder limit.

Choosing the right entity is about more than just numbers; it's about building a foundation that respects your long-term vision. If you're ready to refine your business structure, explore how intentional design can transform your professional landscape.

Integrating Strategy: How Wright CPAs Crafts Your Financial Future

The choice between an S-Corp and an LLC isn't a static decision. It's a foundational element that must support the weight of your growth. At Wright CPAs, we move beyond the mechanical act of filing forms. We focus on business tax planning in Buffalo, NY that anticipates change before it arrives. Our approach treats your business structure as a living design, ensuring your s corp vs llc new york tax strategy remains resilient against shifting state regulations and economic cycles.

Through our CFO services, we monitor the evolution of your entity. We analyze whether your current structure still serves your long-term vision or if it has become a constraint. Accuracy is our baseline. We ensure your business tax preparation in Buffalo aligns perfectly with your chosen entity, eliminating the friction often found between intent and execution. By utilizing a fixed-fee relationship, we provide the spatial breathing room needed for ongoing dialogue without the distraction of hourly billing. This clarity allows you to focus on the craft of your business while we maintain the integrity of its financial framework.

Intentional Tax Strategy for WNY

We begin by analyzing the unique "site" of your business. Just as an architect studies the topography and light of a physical location, we examine your cash flow, payroll requirements, and risk profile. This site-specific analysis determines whether an LLC or an S-Corp provides the most efficient shelter for your assets. The s corp vs llc new york tax debate often centers on the 15.3 percent self-employment tax, but our strategy goes deeper. We facilitate a constant dialogue between your bookkeeping, payroll, and tax strategy. This integration elevates the human experience by removing the frantic anxiety of tax deadlines. When the structure is sound, the pressure dissipates.

Your Next Steps in Buffalo, Rochester, or Syracuse

A structure only remains stable through consistent stewardship. Establishing a year-round relationship with your tax preparer in Buffalo, NY is the most effective way to ensure your entity choice remains optimal as New York updates its tax codes, such as the recent adjustments to the Pass-Through Entity Tax (PTET) rates. We invite you to schedule a consultation to review your current entity architecture. Together, we'll design a transition plan for the upcoming tax year that honors your hard work and protects your future.

- Review your current net income to evaluate S-Corp viability.

- Assess the impact of New York State's specific filing fees on your bottom line.

- Synchronize your owner's draw and payroll for maximum efficiency.

Architecting a Legacy for Your Buffalo Enterprise

The choice between an s corp vs llc new york tax structure isn't merely an administrative task. It's an act of deliberate design. Selecting the right entity provides the tectonic strength needed to support a professional practice navigating the 2024 fiscal landscape. You've explored how New York compliance requirements and pass-through taxation impact your firm's materiality. A structure optimized for New York State Department of Taxation and Finance guidelines ensures that your financial resources remain aligned with your long-term vision. It's about creating a spatial balance between immediate cash flow and future stability.

Wright CPAs brings specialized expertise to Buffalo law firms and professional practices. We integrate modern technology with local Western New York craft to provide a fixed-fee monthly advisory. This model offers predictable financial clarity without the noise of traditional billing. We view tax strategy as a dialogue between your current site and your future structure. Every decision aims at elevating the human experience within your business. You deserve a partner who values substance over spectacle.

Begin a dialogue with Wright CPAs to design your optimal tax structure.

Your business is a permanent intervention in the Buffalo landscape. Let's ensure its foundation is as resilient as the city itself.

Frequently Asked Questions

Is an S-Corp always better than an LLC for taxes in New York?

An S-Corp isn't inherently superior; the choice depends on the specific scale and materiality of your business income. While an LLC offers simplicity, an S-Corp structure can reduce self-employment taxes once profits exceed approximately $60,000. This decision requires a dialogue between your current revenue and your long term vision for the firm. It's about finding the point where administrative craft meets tax efficiency.

What is the "Reasonable Salary" requirement for NY S-Corps?

The IRS requires S-Corp owners to pay themselves a salary that reflects the market value of their craft. This "reasonable compensation" must align with Bureau of Labor Statistics data for similar roles in the Buffalo Niagara region. If an architect earns $90,000 annually in a comparable firm, the IRS expects a similar figure. It ensures the tax structure remains grounded in economic reality rather than mere abstraction.

How much does it cost to form an LLC in Buffalo, NY, including publication?

Forming an LLC in Buffalo requires a $200 filing fee paid to the New York Department of State. You must also satisfy the site-specific publication requirement by placing notices in two newspapers designated by the Erie County Clerk for six consecutive weeks. In Buffalo, these publication costs typically range from $150 to $250. This initial investment establishes the legal foundation of your professional practice within the local vernacular.

Can I change my LLC to an S-Corp later in the year?

You can elect S-Corp status for your LLC, but the timing must be precise. IRS Form 2553 must be filed within 75 days of the start of the tax year or the date of formation. If you miss this window, the change usually takes effect the following year. It's a deliberate transition that requires careful integration with your existing accounting cycles to ensure a seamless spatial shift in your tax obligations.

Does New York State recognize federal S-Corp status automatically?

New York State doesn't recognize federal S-Corp status automatically. You must file Form CT-6 with the Department of Taxation and Finance to ensure your state tax treatment mirrors your federal election. Failing to submit this form results in your business being taxed as a standard C-Corp at the state level. This administrative step is essential for maintaining a cohesive s corp vs llc new york tax strategy that honors your firm's intent.

What are the annual filing fees for an LLC in New York State?

New York LLCs must pay an annual filing fee based on their gross income from the previous year. For businesses with New York source income between $1 and $100,000, the fee is $25. This fee can scale up to $4,500 for firms with income exceeding $25,000,000. It's a recurring obligation that supports the legal framework of your business's place in the state's economic landscape.

How does the NYS Pass-Through Entity Tax (PTET) affect my choice?

The NYS Pass-Through Entity Tax allows S-Corps and LLCs to pay state income tax at the entity level. This creates a federal deduction that bypasses the $10,000 SALT cap established in 2017. For a Buffalo business owner in the 35 percent federal bracket, this can result in thousands of dollars in annual savings. It adds a layer of sophistication to the s corp vs llc new york tax comparison.

What happens if I fail to meet the New York publication requirement?

Failure to complete the publication requirement within 120 days of formation leads to the suspension of your right to conduct business. While the state doesn't typically dissolve the entity immediately, it limits your ability to maintain legal standing in New York courts. This requirement is a tectonic element of New York law. Ignoring it weakens the structural integrity of your liability protection and your firm's professional standing.