What if the strength of your next expansion depended less on your current revenue and more on the structural integrity of your financial records? In a city like Syracuse, where the economic landscape is shifting toward high-tech manufacturing and infrastructure, capital is the foundation of every lasting structure. Yet, many entrepreneurs find getting a business loan ready Syracuse feels like building on sand because of disorganized bookkeeping or technical uncertainty.

It's natural to feel a sense of anxiety when facing the precise requirements of lenders or the nuances of the New York State Commercial Finance Disclosure Law. You deserve a financial foundation that reflects the quality of the work you do every day. This guide provides a sophisticated framework for preparing your capital request, moving beyond simple paperwork to create a curated, bankable narrative. We'll explore how to align your internal KPIs with lender priorities, ensuring you approach every meeting with the quiet confidence of a master builder.

Key Takeaways

- Understand how the shifting Syracuse economic landscape influences lender expectations and how to position your business within this regional growth corridor.

- Master the essential documentation required for getting a business loan ready Syracuse, focusing on the harmony between your tax returns and internal financial statements.

- Identify the critical metrics, such as the Debt Service Coverage Ratio, that lenders use to evaluate the structural integrity of your capital request.

- Follow a methodical application blueprint that includes a three-year financial audit and a review of your business formation documents for total operational clarity.

- Leverage professional CFO services and cash flow management to transition from securing capital to executing a long-term strategy for sustainable expansion.

The Landscape of Business Capital in Central New York

Syracuse is undergoing a period of significant economic renewal. The regional GDP reached $51 billion in 2023; today, that growth is fueled by the I-81 viaduct project and a burgeoning high-tech manufacturing sector. This transformation isn't merely a change in statistics. It's a fundamental reshaping of the city’s commercial foundation. For local firms, this environment presents a unique opportunity to secure growth capital. However, the process of getting a business loan ready Syracuse has evolved. Lenders no longer prioritize volume over substance. They seek businesses that demonstrate a clear, intentional relationship with their financial data.

Local institutions like SECNY and Cooperative Federal Credit Union value a curated approach to financing. They look for a narrative that matches the technical precision of a balance sheet. When exploring various types of business loans, it becomes clear that the most favorable terms go to those who treat their financials as a blueprint rather than a burden. This shift from reactive bookkeeping to proactive capital positioning is essential. It moves the conversation from what happened to what is possible.

Why Readiness Matters in the Syracuse Market

In a high-demand market, time is a finite resource. A well-prepared application acts as a streamlined path through the complexities of the lending process. It reduces the time-to-funding by eliminating the back-and-forth of clarifying disorganized records. Beyond the technical benefits, there's a profound emotional serenity in readiness. Entering a lender meeting with a curated financial package allows you to speak with authority. You aren't just asking for money; you're inviting a partnership in a well-designed future.

The Role of Financial Intentionality

Sophistication begins with the rejection of the shoebox mentality. A professional financial system provides the sensory detail lenders need to feel confident in your vision. This intentionality extends to tax planning and strategy. By aligning your tax obligations with your growth goals, you demonstrate a rigorous commitment to fiscal excellence. Loan readiness is a state of structural financial health where every figure supports the overall integrity of the enterprise. It's the moment your bookkeeping becomes a strategic asset.

Designing Your Financial Foundation: The Essential Documents

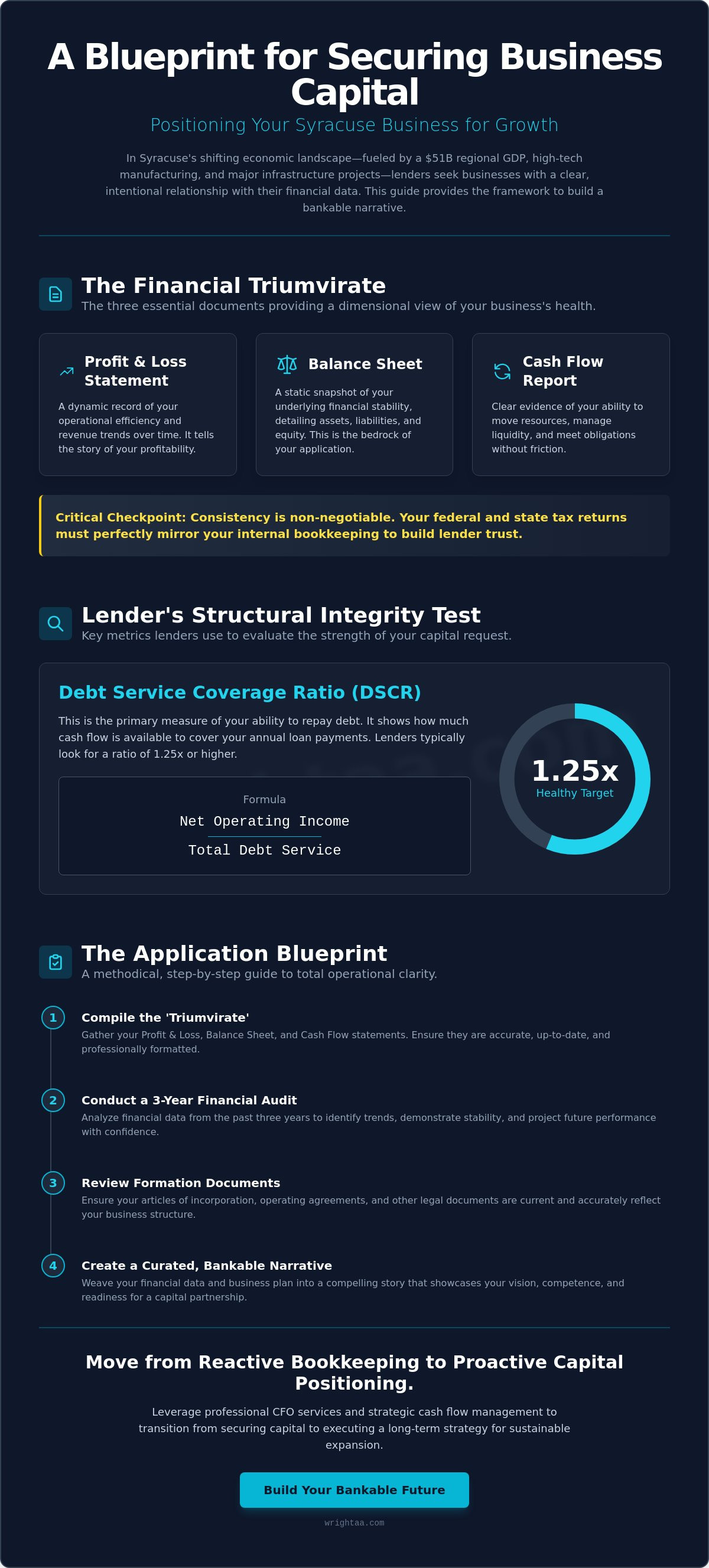

Every architectural masterpiece begins with a set of precise drawings. In the context of getting a business loan ready Syracuse, these drawings are your financial statements. Lenders look for a "Triumvirate" of documents that provide a three dimensional view of your business’s health:

- Profit & Loss Statement: A record of your operational efficiency and revenue trends over time.

- Balance Sheet: A snapshot of your underlying financial stability and equity.

- Cash Flow Report: Evidence of your ability to move resources through the system without friction.

Consistency across these documents is non negotiable. Your federal and state tax returns must mirror your internal bookkeeping. Discrepancies create doubt; doubt creates rejection. When you review SBA loan eligibility requirements, you'll see that transparency is the first hurdle. Modern bookkeeping technology helps achieve this by creating a tactile sense of trust. It allows lenders to see that your data is grounded in real time reality rather than manual guesswork.

The Precision of the Balance Sheet

Your balance sheet is often the most scrutinized document in any application. It's the bedrock. Lenders examine it to understand your debt to equity ratio and the liquidity of your assets. It's vital to clean up any "noise" before submission. This includes resolving long standing shareholder loans or ensuring that asset valuations reflect current market truths. For a deeper look at these foundational principles, explore our guide on small business accounting in Buffalo, NY: designing financial clarity. A clean balance sheet signals that your business is built on solid ground.

Specialized Requirements for Law Firms and LLCs

Law firms and professional practices in Syracuse face unique documentation hurdles. For attorneys, IOLTA compliance is more than a regulatory requirement. It's a signal of extreme financial discipline. Lenders look for three way reconciliation between bank statements, client ledgers, and the general ledger. This level of detail proves that you manage capital with the same care you apply to your clients' cases.

Closely held businesses must also be intentional about how they present distributions versus reinvested capital. A lender needs to see that the business retains enough earnings to support new debt. If you're looking to refine your practice's financial narrative, consider the insights in our article on CPA for law firms in Buffalo, NY: elevating your practice through financial intentionality. Establishing this level of meticulous bookkeeping ensures your loan application is viewed as a blueprint for success rather than a risk.

Structural Integrity: What Syracuse Lenders Look for Beyond the Numbers

A building’s beauty is superficial if its frame cannot support its weight. Lenders view your business through a similar lens of structural integrity. Beyond the stack of documents, they analyze the mechanics of your repayment capacity. The primary metric for this is the Debt Service Coverage Ratio (DSCR). It's a simple yet profound calculation of your net operating income against your total debt obligations. A ratio above 1.25 often signals a healthy margin of safety. When you're getting a business loan ready Syracuse, understanding this number is like knowing the load bearing capacity of your foundation.

Modern lenders also apply the "Five Cs of Credit," but they interpret them with newfound sophistication. Character is no longer just a handshake; it's the consistency of your reporting. Capacity is your operational agility. Capital is the equity you've invested in your vision. Collateral provides the physical security for the risk. Conditions represent the external environment, from interest rates to local economic shifts. By identifying and addressing potential red flags in these areas early, you maintain control of the narrative. You ensure that the lender sees the strength of the structure rather than the dust of the construction site.

The Narrative of Cash Flow

Cash flow is the breath of an organization. In Syracuse, this rhythm often follows seasonal patterns, from the quiet of lake effect winters to the vibrant activity of the university cycles. Proactive cash flow management serves as a buffer against these fluctuations. It demonstrates to a lender that you understand the specific geographic context of your market. You aren't just surviving the seasons; you're designing around them. This level of foresight transforms a simple spreadsheet into a compelling story of stability.

Debt-to-Income and Structural Ratios

Your current leverage dictates your future freedom. Lenders prefer a steady, predictable financial rhythm over sporadic bursts of growth that lack a solid base. Calculating your current debt to income ratio allows you to see what the bank sees before you step into the meeting. If your past contains financial challenges, don't obscure them. Instead, present a narrative of resilience. Show how those experiences led to more rigorous internal controls and better financial intentionality. This transparency builds a bridge of trust. It proves that your business possesses the structural resilience to handle new capital responsibly.

The Application Blueprint: A Step-by-Step Preparation Guide

The path to capital is a sequence of intentional movements. It's the transition from financial theory to tangible execution. For Syracuse entrepreneurs, the process of getting a business loan ready Syracuse is most effective when it follows a rigorous, step by step blueprint. This isn't a race toward a signature. It's a patient assembly of facts and vision.

- Step 1: Conduct a comprehensive internal financial audit of the last three years to ensure every trend is understood.

- Step 2: Align your business formation documents with your current reality, ensuring legal structures match operational growth.

- Step 3: Develop a three year financial projection that balances visionary goals with historical data.

- Step 4: Curate a professional summary of the loan's specific purpose and the projected ROI.

- Step 5: Review the entire package with a strategic advisor to ensure total alignment between your narrative and your numbers.

Developing Visionary Projections

Forecasts are often dismissed as best guesses. In a sophisticated application, they are data driven revenue and expense models. Your strategic plan should breathe through the numbers on the page. Syracuse lenders, particularly those watching the growth in manufacturing and high tech sectors, respect conservative targets. They value a well defended growth plan over an optimistic one that lacks a base. Your projections should explain how external factors, like regional infrastructure projects or the I-81 corridor development, will influence your internal performance.

The Final Review: Aesthetic and Technical Accuracy

The presentation of your data matters as much as the data itself. Every document should be formatted with the professional clarity of a design firm. This aesthetic discipline suggests a corresponding operational discipline. Check for dualities. Do your tax returns match your internal P&L statements exactly? Any friction here can stall an application. A "CFO level" final walkthrough provides the necessary distance to see your business as a lender does. If you need assistance refining your financial narrative, our business consulting services can help bridge the gap between your current records and a bankable package. This final step transforms a collection of data into a cohesive, authoritative blueprint for growth.

Partnering for Growth: How Strategic Accounting Secures Your Future

Capital acquisition is a significant milestone, yet it's merely the commencement of a deeper narrative. In the journey of getting a business loan ready Syracuse, many entrepreneurs view the bank's approval as a final destination. A more sophisticated perspective recognizes that a loan is the beginning of a long term relationship with your financial structure. This capital is a raw material. Its ultimate value is determined by the precision with which it's deployed and managed over the coming years. Securing the funds is the first step; stewardships of those funds is what builds a legacy.

Strategic accounting provides the necessary oversight to ensure this new foundation remains stable. Wright CPAs, LLC offers the architecture of finance for Syracuse firms, moving beyond basic compliance to provide visionary guidance. This partnership ensures that your financial environment remains healthy, transparent, and resilient long after the initial funding has arrived. It's the transition from mere readiness to a state of permanent financial clarity, where every fiscal decision supports the overall design of the enterprise.

Beyond the Approval

The period following a loan disbursement requires a disciplined approach to monitoring and reporting. Lenders often include specific covenants and reporting requirements that act as the structural supports for the lending agreement. Maintaining these with professional precision is essential for preserving your reputation and your future borrowing capacity. Strategic reinvestment is equally vital. It's the process of using your new resources to improve daily operations and build long term value. For many growing firms, outsourced CFO services provide the high level oversight needed to manage these complex dynamics effectively.

A Commitment to Design Excellence

The philosophy at Wright CPAs, LLC is rooted in deep listening and contextual awareness. We understand that your business is an intervention in the local economy, much like a building is an intervention in the landscape. Our approach favors substance over spectacle. Through fixed fee retainers, we provide ongoing oversight, bookkeeping, and cash flow management. This ensures that your growth is both sustainable and intentional. This commitment to design excellence allows you to focus on your craft while we maintain the integrity of your financial foundation. Begin your journey toward financial clarity with a consultation and discover how a curated financial strategy can secure your future.

Building a Legacy of Financial Stability

Capital is the bridge between a visionary concept and its physical reality. In Central New York, this bridge requires a foundation of technical accuracy and strategic foresight. You've seen that the process of getting a business loan ready Syracuse involves more than just gathering paperwork. It requires a curated narrative where your balance sheet and cash flow reports speak to the structural integrity of your enterprise. By aligning your internal bookkeeping with external lender priorities, you transform a technical requirement into a strategic advantage.

Since 2012, Wright CPAs, LLC has approached financial management with professional discipline and a specialized focus on Law Firm and LLC accounting. We believe clarity should be a permanent fixture of your operations, not a temporary state. Our fixed-fee monthly advisory retainers ensure you have the ongoing oversight needed to navigate complex capital landscapes with confidence. Your business deserves a foundation built to last. Design your path to capital with a strategic consultation. We look forward to helping you build a future that's both grounded and visionary.

Frequently Asked Questions

What are the most common financial documents required for a business loan in Syracuse?

Profit and Loss statements, Balance Sheets, and Cash Flow statements form the core of your technical package. Lenders also require three years of business and personal tax returns, a schedule of existing liabilities, and your formation documents. These records provide a three dimensional view of your firm’s historical performance and its structural stability.

How far back should my tax returns go when applying for a small business loan?

Lenders in Central New York typically require the last three years of business and personal tax returns to establish a reliable performance trend. This history allows them to observe consistency and resilience across different economic cycles. If your business has operated for less than three years, you should provide all available returns alongside comprehensive interim statements for the current fiscal year.

Can I get a business loan if my personal credit score is not perfect?

Yes, it's possible to secure capital with a less than perfect score by demonstrating strong business cash flow and offering tangible collateral. While credit scores are a component of the decision, lenders also evaluate your character and the capacity of the business to service debt. Professional bookkeeping and a clear narrative can help mitigate concerns regarding personal credit history.

What is the difference between a term loan and a business line of credit for Syracuse firms?

A term loan provides a lump sum for a specific investment, whereas a line of credit offers revolving access to capital as needed. Term loans are suited for permanent interventions like equipment or real estate. Lines of credit are better for managing the rhythmic fluctuations in cash flow that often accompany the seasonal nature of the Syracuse market.

How long does the business loan preparation process typically take with a CPA?

The preparation process usually spans four to eight weeks depending on the current state of your financial records. Getting a business loan ready Syracuse requires a methodical audit of your bookkeeping and the curation of data driven projections. This unhurried approach ensures that your final application package possesses the technical precision required to inspire lender confidence.

Why do Syracuse lenders care about my debt service coverage ratio (DSCR)?

Lenders use the DSCR to verify that your business generates sufficient net operating income to comfortably meet its debt obligations. It's a primary indicator of your repayment capacity and operational health. A ratio above 1.25 suggests a healthy margin of safety, proving your business can sustain its growth without compromising its underlying financial integrity.

Should I apply for an SBA loan or a conventional bank loan?

SBA loans generally offer lower down payments and longer repayment terms, while conventional loans may provide a more streamlined closing process. Your choice depends on your specific needs for leverage and the urgency of your project. SBA programs are often an excellent choice for businesses that possess strong cash flow but lack traditional levels of collateral.

How do I present my business projections if I am a new startup in Syracuse?

Startup projections must be grounded in rigorous market research and realistic industry benchmarks. Focus on explaining the specific logic behind your revenue targets and expense forecasts rather than offering optimistic guesses. Detailed cash flow management plans demonstrate to lenders that you possess the discipline to navigate the early, often volatile stages of a new enterprise.