A law firm is more than its active cases; it's a structure built on the quiet integrity of its financial foundations. In New York, the distinction between legal counsel and financial stewardship often feels blurred, leaving many partners with a persistent anxiety regarding trust account audits. Effective tax planning for law firms NY isn't merely about meeting a deadline or calculating the 2.25% IOLA safe harbor rate. It's about designing a deliberate financial environment that allows your practice to breathe with purpose.

You likely entered the legal profession to advocate for your clients, not to spend your evenings untangling complex state tax regulations or the rigid seven-year recordkeeping mandates of Rule 1.15. This guide, brought to you by Wright CPAs, LLC, offers a serene, repeatable framework that transforms compliance from a burden into a source of operational clarity. We'll examine the specific structural requirements of New York accounts alongside proactive tax strategies that provide peace of mind and support the long-term growth of your firm.

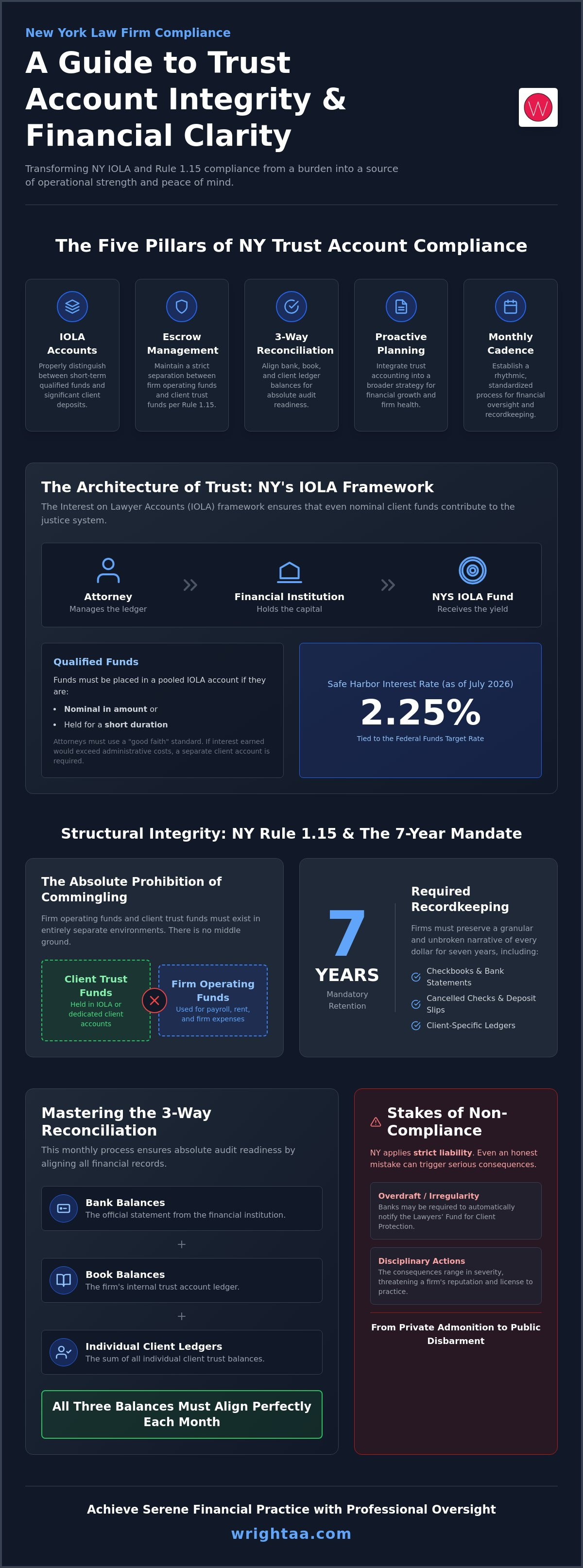

Key Takeaways

- Understand the structural role of New York IOLA accounts to clearly distinguish between qualified short-term funds and significant client deposits.

- Implement a rigorous blueprint for escrow management based on NY Rule 1.15 to ensure firm operating funds remain entirely distinct from client trust funds.

- Master the 3-way reconciliation process to align bank balances, book balances, and individual client ledgers for absolute audit readiness.

- Discover how proactive tax planning for law firms NY integrates trust accounting into a broader strategy for financial growth and operational clarity.

- Establish a rhythmic monthly cadence for financial oversight that standardizes the intake process and removes the friction of manual recordkeeping.

The Architecture of Trust: Understanding the IOLA Framework in New York

The financial integrity of a New York practice begins with how it handles money that doesn't belong to it. This responsibility is codified through the Interest on Lawyer Accounts (IOLA) framework. It's a vital component of the state's legal aid infrastructure. When a firm holds client funds that are too small or held for too short a time to generate net interest for the individual, those funds must reside in a pooled IOLA account. The interest generated doesn't enrich the firm or the bank; it supports civil legal services for low-income New Yorkers.

Effective tax planning for law firms NY requires a deep understanding of these boundaries. You aren't simply moving numbers. You're maintaining the ethical walls of your firm. New York strictly prohibits non-interest-bearing accounts for client funds. Every dollar must be active and accounted for. The relationship is a triad. The attorney manages the ledger. The financial institution holds the capital. The NYS IOLA Fund receives the yield. This structure ensures that even nominal deposits contribute to the broader justice system while protecting the client's principal.

The yield on these accounts is not static. As of July 2026, the Safe Harbor interest rate for participating banks is 2.25%. This rate, tied to the Federal Funds Target Rate, ensures that the interest generated remains meaningful. For the firm, the IOLA account acts as a temporary reservoir. It requires a disciplined approach to bookkeeping to ensure that these funds never mix with the firm's operating capital. Clarity here is the first step toward a serene financial practice.

What Constitutes Qualified Funds in NY?

Determining which funds belong in a general IOLA account requires professional judgment. New York defines "qualified funds" as those that are nominal in amount or held for a short duration. There's no hard dollar limit. Instead, attorneys must apply a "good faith" standard. If a deposit is large enough or will be held long enough to generate interest that exceeds the cost of administering a separate account, it must be placed in a dedicated, interest-bearing account for that specific client. Misclassifying these funds can lead to lost value for the client or administrative friction for the firm.

The Consequences of Non-Compliance

Precision is not optional. New York applies a standard of strict liability to the commingling of funds. Even an honest mistake can trigger a chain of events that disrupts your practice. If an account is overdrawn or if irregular activity occurs, the bank is often required to provide an automatic notification to the Lawyers’ Fund for Client Protection. Disciplinary actions are serious; they range from private admonitions to public disbarment. Integrating these requirements into your broader tax planning for law firms NY ensures that your firm's growth is never compromised by avoidable oversight.

Structural Integrity: Mandatory Recordkeeping and NY Rule 1.15

Rule 1.15 of the New York Rules of Professional Conduct is more than a list of restrictions. It is the architectural blueprint for escrow management. It defines the boundary between the firm's operational survival and its ethical standing. Central to this rule is the absolute prohibition of commingling. Firm operating funds and client trust funds must exist in separate environments. There is no middle ground. Even a temporary overlap of these assets constitutes a violation of the firm’s structural integrity.

The responsibility of access is equally critical. Authorized signatories should be limited to those with a deep understanding of these ethical stakes. Access isn't merely a clerical task; it's a form of high-level stewardship. This clarity in access ensures that every movement of capital is intentional and documented. Integrating these practices into your broader tax planning for law firms NY creates a foundation that supports both compliance and long-term profitability.

New York’s 7-Year Recordkeeping Rule

New York mandates a rigorous retention period. Rule 1.15(d) requires that specific financial records be preserved for seven years. This isn't a suggestion; it's a requirement for permanence. Required documents include checkbooks, bank statements, cancelled checks, and duplicate deposit slips for every transaction. The ledger must be granular. Every receipt and disbursement must be tracked specifically by the client's name. In a modern firm, digital records are acceptable, provided they remain accessible and secure. The goal is an unbroken narrative of every dollar's journey through your practice. Establishing a cadence of compliance ensures these records are updated in real-time rather than reconstructed during a stressful audit.

The Trap of Cashing Out Earned Fees

A common friction point arises when fees are earned. The proper procedure involves a prompt transfer from the trust account to the operating account once the work is complete and the fee is undisputed. Leaving earned fees in a trust account for an extended period creates a state of commingling. The funds are now yours, yet they reside in a client space. Conversely, if a client disputes a fee, the disputed portion must remain in the trust account until the matter is resolved. This duality requires constant vigilance and a predictable system for fee realization. It’s a delicate balance that requires professional oversight to ensure that your firm’s cash flow remains healthy without crossing ethical lines.

Mastering the 3-Way Reconciliation Process

Financial alignment in a law practice is a quiet, rhythmic virtue. While a standard two-way reconciliation compares a bank statement to a firm’s internal books, it's an incomplete measure of health for a legal practice. In the context of New York's IOLA program, the three-way reconciliation serves as the architectural validation of your firm’s ethical and fiscal structure. It requires that the bank balance, the firm’s book balance, and the sum of all individual client ledgers reach a state of perfect symmetry. This process is the CFO-level heartbeat of a firm that values intentionality over reactionary accounting.

Relying solely on a two-way reconciliation is a common risk. A firm might see a bank balance that matches their general ledger and assume all is well. However, this oversight ignores the granular promises made to individual clients. If the total of all client ledgers doesn't match the adjusted bank balance, the firm’s ethical foundation is fractured, even if the total amount of cash is correct. Integrating this level of scrutiny into your broader tax planning for law firms NY ensures that you're not just compliant, but fully aware of the capital flowing through your practice.

The Mechanics of the Three-Way Match

The process begins with Step 1: Reconciling the trust bank statement to your firm’s general ledger. This accounts for outstanding checks and deposits in transit. Step 2 requires summing every individual client ledger to ensure they match that adjusted total. The goal is a zero-sum reality. Every penny in the account must be attributed to a specific client at all times. Accuracy here prevents the slow drift toward confusion that often precedes a trust account audit.

Common Reconciliation Pitfalls for NY Firms

Negative client balances are the cardinal sin of trust accounting. They occur when one client’s funds are inadvertently used to cover another’s expenses, usually due to timing errors or poor ledger tracking. Another frequent friction point is the treatment of bank fees. In New York, the firm must pay for account maintenance from its operating account. Allowing a bank to deduct fees from an IOLA account is a direct violation of Rule 1.15. Finally, handling unidentified funds requires a specific discipline. If a "mystery" deposit appears, it cannot simply be absorbed into firm income; it must be investigated and properly classified to maintain the integrity of the ledger. Professional tax planning for law firms NY treats these reconciliations as a monthly ritual of clarity, clearing away errors before they become ethical liabilities.

A Cadence of Compliance: Monthly Protocols for NY Law Practices

A firm's stability is found in its repetition. Much like the maintenance of a physical structure, financial compliance requires a steady, unhurried rhythm. Establishing a monthly cadence for trust account oversight ensures that minor discrepancies don't evolve into structural failures. This discipline is a core component of tax planning for law firms NY, transforming ethical requirements into a predictable operational flow. It's not enough to react to problems; a healthy practice designs systems that prevent them from arising.

Training administrative staff on strict escrow protocols is an essential investment in this foundation. Every member of the team must understand that these accounts are not merely bank accounts but sacred trusts. For firms seeking Small Business Accounting in Buffalo, NY, the goal remains the same: achieving a level of financial clarity that supports growth without sacrificing peace of mind. This clarity begins with the intake of a single retainer and extends to the final disbursement of a case.

Monthly and Quarterly Review Procedures

The 3-way reconciliation must be performed and signed off on every 30 days without exception. This monthly review should also include a scan for stale-dated checks. In New York, funds that remain unclaimed for long periods are subject to escheatment laws. You must identify these abandoned funds early to follow the proper legal channels for their disposition. Quarterly, partners should spot-check individual client ledgers for unexpected activity. These internal controls act as a safeguard, ensuring that the firm's financial narrative remains accurate and honest.

Intake and Disbursement Best Practices

Standardizing the intake process is where compliance begins. All trust deposits must be directed into IOLA-approved banks in New York. This ensures the interest reaches the intended state funds. A critical protocol is the Cleared Funds rule. Never make a disbursement until the underlying deposit has fully cleared the banking system. This patience prevents the accidental use of other clients' capital. Maintaining a meticulous paper trail is mandatory. Rule 1.15 essentially prohibits ATM and cash transactions for trust accounts because they lack the transparency required for legal escrow. Every movement of money must be documented with precision.

If you're ready to move beyond manual recordkeeping and implement a professional financial system, explore our Law Firm Accounting services to bring order to your practice.

Strategic Intentionality: How Professional Oversight Elevates Your Firm

Professional oversight is a deliberate choice to prioritize quality over volume. In an age where automated bookkeeping promises ease, the human element remains the most critical safeguard for a law practice. Software can track a transaction, but it cannot interpret the ethical nuance of New York's legal landscape. Moving from a state of compliance fear to one of financial intentionality requires a partner who understands the intersection of accounting and legal ethics. Wright CPAs, LLC integrates trust accounting into a proactive financial strategy, ensuring your firm's foundation is as resilient as its reputation.

This approach transforms tax planning for law firms NY from a defensive necessity into a visionary tool. When your books are curated with precision, you gain the freedom to look forward. You no longer wait for an audit to discover a discrepancy. Instead, you operate with the quiet confidence that every dollar is exactly where it should be. This level of clarity isn't just about avoiding disciplinary action; it's about building a practice that reflects your commitment to excellence. It's the difference between a structure that merely stands and one that is built to endure.

Fixed-Fee Advisory for Law Firms

Predictability is the cornerstone of a calm practice. A fixed-fee monthly advisory model removes the friction of hourly billing for financial oversight. It provides a steady cadence for ongoing trust account reconciliation and proactive reporting. This model allows for sophisticated tax planning strategies that account for the unique cash flow patterns and partner draws inherent in legal work. By utilizing Outsourced CFO Services in Buffalo, NY, firms can navigate complex city-specific taxes, such as the 8.85% NYC General Corporation Tax, with strategic foresight rather than last-minute panic. It ensures that your tax strategy is as intentional as your case strategy.

The Intersection of Ethics and Efficiency

Modern technology is a powerful instrument, but it requires a disciplined hand. We leverage advanced tools to streamline recordkeeping while maintaining the professional skepticism necessary for human accountability. This balance reduces the administrative burden on partners, allowing them to return their focus to billable work and client advocacy. Working with a specialized CPA for Law Firms Buffalo NY ensures that your financial systems are as rigorous as your legal arguments. Wright CPAs, LLC provides the structural financial clarity that serves as the ultimate competitive advantage. It provides the stability required to scale your firm with purpose and poise, ensuring that your growth is never compromised by an unstable foundation.

Building a Practice of Permanence and Clarity

A firm’s legacy is shaped by the intentionality of its daily operations. By mastering the IOLA framework and the rigorous requirements of Rule 1.15, you move beyond the friction of compliance and into a state of operational serenity. The 3-way reconciliation becomes a rhythmic validation of your firm’s ethical health. This foundation is essential for effective tax planning for law firms NY, allowing you to focus on advocacy while your financial systems remain unshakable.

Wright CPAs, LLC provides the Specialized Law Firm Accounting and CFO-level guidance necessary for firms in Buffalo, Rochester, and Syracuse to thrive. Our fixed-fee monthly retainers offer predictable budgeting, ensuring that your financial oversight is as steady as your counsel. Elevate your law firm’s financial clarity with Wright CPAs, LLC and design a practice that is both profitable and profoundly principled. You've built your firm on expertise; let us provide the structural clarity to sustain its growth.

Frequently Asked Questions

What is the difference between IOLTA and IOLA in New York?

IOLA is the New York-specific term for the Interest on Lawyer Account program. While most other states utilize the acronym IOLTA (Interest on Lawyers' Trust Accounts), the two are conceptually identical. Both systems pool nominal or short-term client funds to generate interest that supports civil legal services for low-income residents, managed specifically by the NYS IOLA Fund.

Can I use a regular business savings account for client funds in NY?

You cannot use a standard savings account for client deposits. New York mandates that these assets reside either in IOLA-approved accounts or in dedicated interest-bearing accounts opened for a specific client's benefit. A regular business account lacks the mandatory interest-remittance structure required by state ethical rules and fails to protect the capital from commingling.

How often must I perform a 3-way reconciliation for my trust account?

A 3-way reconciliation must be completed every 30 days without exception. This rhythmic oversight ensures that your bank statement, internal firm ledger, and the sum of individual client balances remain in perfect symmetry. Consistent monthly reviews are a hallmark of high-level tax planning for law firms NY and provide a serene defense during potential audits.

What happens if I accidentally commingle my own funds with client funds?

Immediate rectification is necessary to preserve the integrity of your practice. You should transfer the misplaced funds and document the correction clearly in your ledger. Because New York follows a standard of strict liability for commingling, even unintentional errors can trigger bank-initiated notifications to the Lawyers’ Fund for Client Protection, potentially leading to a disciplinary review.

Does New York require a specific type of software for IOLTA compliance?

No specific software brand is mandated by New York law. Your chosen system must simply be capable of maintaining detailed, client-specific records and ledgers for the required duration. Many firms choose legal-specific accounting platforms to ensure their bookkeeping naturally aligns with the granular demands of Rule 1.15 and the seven-year retention rule.

How long do I need to keep my law firm’s financial records in NY?

You must preserve your firm's financial records for a minimum of seven years. This mandate, established by Rule 1.15(d), covers bank statements, ledgers, check stubs, and duplicate deposit slips. Maintaining these records is an act of structural integrity, ensuring that every transaction remains transparent and verifiable long after a legal matter has concluded.

Can a non-lawyer be a signatory on an IOLA account in New York?

Non-lawyers may serve as signatories on these accounts, but the attorney bears ultimate ethical responsibility for every transaction. Entrusting a non-lawyer with access requires rigorous internal controls and constant oversight. Many practices prefer to keep signatory authority limited to partners who have a direct stake in the firm's professional standing and compliance.

How does Wright CPAs, LLC help Buffalo law firms with tax planning?

Wright CPAs, LLC offers specialized Law Firm Accounting and CFO-level guidance tailored to the New York legal landscape. We replace stressful, manual recordkeeping with a serene, fixed-fee advisory model that ensures predictable budgeting. The approach provided by Wright CPAs, LLC integrates trust compliance into a broader tax planning for law firms NY strategy, supporting intentional growth for firms in Buffalo, Rochester, and Syracuse.