What if the regulatory mandates often viewed as burdens were actually the blueprints for your firm's financial resilience? In a state where high corporate liability can feel like an immovable force, the strategic use of NY small business tax credits offers a way to reclaim your agency. You understand that managing a business in Western New York requires a balance between honoring your team and protecting your bottom line. The complexity of the SECURE 2.0 updates and the approaching NY Secure Choice deadlines can feel overwhelming, yet they provide a rare opening to build a more intentional foundation.

You'll discover how to transform retirement planning from a technical exercise into a structural tax advantage. This guide explains how to utilize federal incentives to offset 100% of startup costs and leverage employer contribution credits to lower your annual bill. We'll walk through the specific 2026 registration timelines for the state mandate and the precise mechanisms that turn compliance into a tool for attracting talent and achieving lasting financial clarity.

Key Takeaways

- Identify the distinction between tax deductions and credits to treat your financial strategy as a structural asset rather than a seasonal obligation.

- Learn how to claim up to $5,000 annually for three years through federal startup cost credits, effectively neutralizing the initial cost of a new retirement plan.

- Navigate the 2026 registration deadlines for the NY Secure Choice mandate while utilizing NY small business tax credits to transform regulatory compliance into a competitive benefit.

- Evaluate the minimalist design of a SEP IRA against the balanced participation of a SIMPLE IRA to find the retirement framework that aligns with your specific business goals.

- Discover how a year-round advisory model provides the financial clarity and intentionality required to master New York’s complex tax environment.

The Architecture of Tax: Understanding Credits as Structural Assets

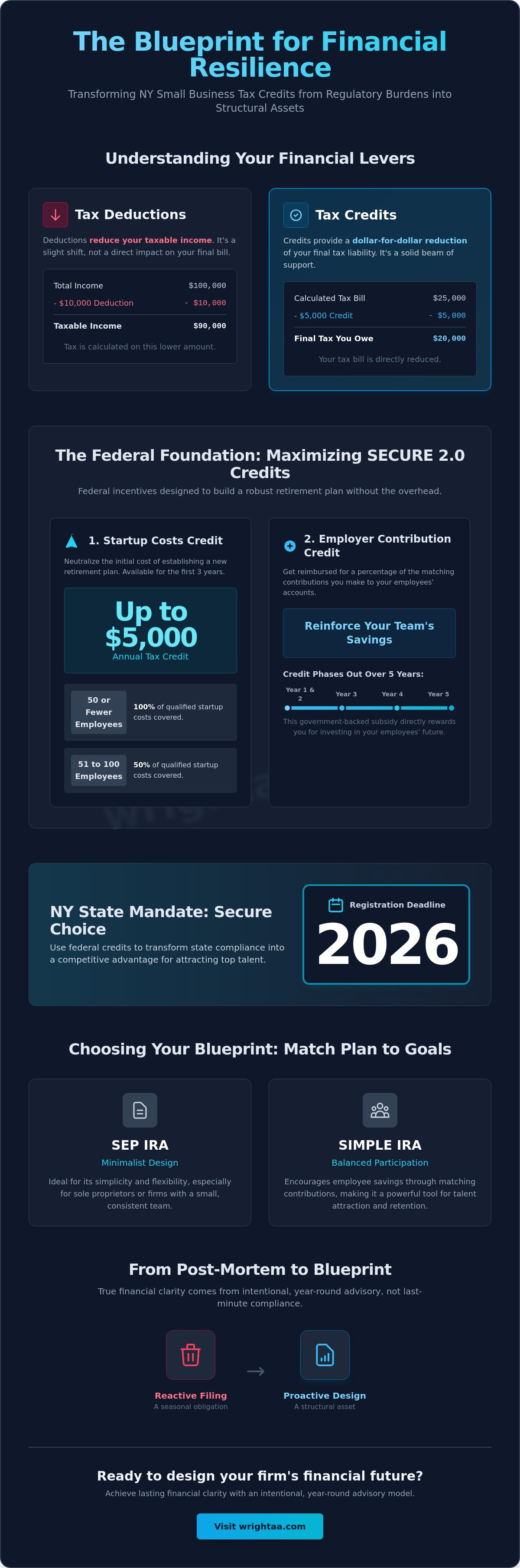

A building's strength depends entirely on its foundation. In the financial life of a firm, tax planning serves a similar purpose. Many business owners view taxes as a seasonal erosion of capital. They focus on deductions, which merely lower the income subject to taxation. However, NY small business tax credits function differently. They are structural interventions. A credit provides a dollar-for-dollar reduction in your total liability. If a deduction is a slight shift in the terrain, a credit is a solid beam that supports the entire frame. It's a direct subtraction from the bill you owe the government.

The year 2026 represents a unique construction phase for New York entrepreneurs. Legislative shifts, specifically the SECURE 2.0 Act, have introduced new incentives that act as permanent improvements to a business's cash flow. These aren't temporary windfalls. They're intentional tools designed to stabilize the intersection of corporate responsibility and private wealth. By viewing these credits as assets, you move from a reactive posture to a state of quiet authority. You stop merely paying for the past and start investing in the future structure of your company.

Intentionality in Financial Design

A tax return shouldn't be a post-mortem. It's a blueprint. Proactive business tax planning Buffalo NY allows you to identify these credits before the ground is even broken on a new fiscal year. Waiting until April to consider your strategy is a design failure. It leaves the structure of your business vulnerable to the elements of high state liability. True financial clarity requires deep listening and contextual awareness of the tax code long before the filing deadline. When you plan with intention, the tax return becomes a map of your firm's growth and resilience.

The Dual Value of Retirement Credits

Retirement credits offer a duality of purpose. On the surface, they lower the immediate cost of business operations. They provide the liquidity needed to maintain daily momentum. Beneath that layer, they build a foundation for the owner's personal financial serenity. In the Western New York market, these benefits also serve an environmental function. They help you attract a higher caliber of talent by offering a more sophisticated benefits package. When a retirement plan is funded by NY small business tax credits, the business achieves a rare balance. It honors the human element while maintaining a rigorous commitment to fiscal excellence.

The Federal Foundation: Maximizing SECURE 2.0 Credits in 2026

The federal landscape provides the primary materials for your financial foundation. With the implementation of the SECURE 2.0 Act, the government has shifted from merely suggesting retirement participation to actively subsidizing the design. This legislation acts as a structural support for NY small business tax credits, allowing firms to build robust benefits without the traditional weight of administrative overhead. It is a visionary approach to the intersection of labor and capital. These credits are not merely rebates; they are the government's investment in the permanence of your business's retirement structure.

The Startup Costs Credit (Form 8881)

Establishing a new retirement plan involves initial friction and technical setup. The startup costs tax credit addresses this directly by neutralizing the financial barrier to entry. Eligibility requires having 100 or fewer employees who received at least $5,000 in compensation in the preceding year. For businesses with 50 or fewer employees, the credit covers 100% of qualified startup costs up to $5,000 per year. Larger firms with 51 to 100 employees can claim 50% of these costs. This incentive remains available for a three-year window following the plan's inception to ensure the new structure has time to settle.

Subsidized Matching Contributions

The legislation also introduces a significant subsidy for employer matching, functioning as a government-backed reinforcement for your staff's savings. This credit reimburses a percentage of the contributions you make to your employees' accounts over a five-year period. For businesses with 50 or fewer employees, the credit covers 100% of contributions for the first two years, eventually phasing down to 25% by the fifth year. This subsidy is capped at $1,000 per employee annually. These benefits are reduced for WNY businesses with 51 to 100 employees and exclude contributions for highly compensated individuals to maintain a focus on broad-based equity.

Modernizing your participation through automatic enrollment provides an additional layer of support. Firms that add this feature receive a $500 credit per year for three years. These incentives work together to lower the barrier for your team's financial security. If you're looking to align these federal benefits with your specific business goals, a refined tax strategy can help ensure every component is properly placed. By integrating these credits, you create a space where growth is both sustainable and serene.

New York Specifics: Secure Choice and the Subtraction Modification

New York's regulatory landscape requires a precise touch. While federal incentives provide the general foundation, state-level mandates dictate the immediate timeline for compliance. For many, the intersection of these two forces is where the most significant NY small business tax credits are discovered. It is a matter of choosing a path that fulfills a legal requirement while simultaneously reinforcing the business's capital. In the commercial corridors of Buffalo, Rochester, and Syracuse, this choice defines the difference between a reactive expense and a proactive asset.

The Secure Choice Mandate vs. Private Plans

The New York Secure Choice Savings Program is now a reality for private-sector employers with 10 or more employees. If you've been in business for at least two years and don't offer a qualified plan, participation is mandatory. The registration deadlines are approaching quickly in 2026. Employers with 30 or more staff must register by March 18. Those with 15 to 29 employees have until May 15; the smallest firms of 10 to 14 must act by July 15. The program is an automatic enrollment Roth IRA, but it carries a specific limitation: employers cannot contribute to it.

Because the state program prohibits employer contributions, it offers no access to the federal tax credits that offset startup costs or matching funds. Establishing a private 401(k) or SIMPLE IRA exempts you from the mandate and unlocks the incentives discussed earlier. Integrating this choice into your small business accounting Buffalo NY workflow allows you to maintain control over the design of your benefits. Choosing a private structure often provides a more sophisticated equilibrium between meeting state requirements and maximizing federal subsidies.

The NYS Small Business Subtraction Modification

Beyond retirement incentives, New York offers a quiet but effective tool known as the Small Business Subtraction Modification. This isn't a credit, but a structural adjustment to your taxable income. Eligible small businesses can subtract 5% of their net business income from their federal adjusted gross income. For those in the agricultural sector, this subtraction increases to 15%. It's a permanent intervention in how the state views your earnings.

To qualify, a business must be a resident individual, a member of an LLC, or a partner in a firm where the net income is less than $250,000. This modification works in tandem with NY small business tax credits to lower the overall tax burden. It's an often overlooked detail that, when applied correctly, provides a subtle but permanent reduction in state liability. Every element of your financial structure should serve a purpose; this modification ensures that your income is protected at the state level before federal calculations even begin.

Strategic Selection: Matching Plan Types to Business Goals

Choosing a retirement vehicle is an act of design. It requires a deep understanding of your firm's current volume and future aspirations. The right structure doesn't just hold capital; it creates a clear path for NY small business tax credits to flow back into your business. For many in Western New York, the decision rests on the balance between administrative simplicity and the capacity for long-term growth. Every choice is a permanent intervention in your company's financial health.

SEP and SIMPLE IRAs for Small Teams

The SEP IRA is a minimalist tool. It's often the preferred choice for a CPA for law firms Buffalo NY because it allows for significant contributions with almost no administrative weight. It's an ideal fit for solo practitioners or small partnerships where the owner's contribution is the primary focus. For businesses with under 10 employees, the SIMPLE IRA offers a different equilibrium. It carries lower overhead than a full 401(k) while still encouraging employee participation through a mandatory employer match. To secure tax benefits for the 2026 fiscal year, these plans must be established by specific deadlines, typically October 1 for a new SIMPLE IRA.

The 401(k) as a CFO-Level Strategy

When a firm reaches a certain complexity, the 401(k) becomes the most effective structural asset. It offers the highest contribution ceilings and maximum flexibility through curated profit-sharing features. This is a core component of outsourced CFO services Buffalo NY, where the goal is to reduce corporate tax liability while rewarding key staff members. The 401(k) allows for the highest level of individual tax deferral for owners. For growing Buffalo firms, Safe Harbor provisions simplify the compliance process by bypassing traditional non-discrimination testing. This ensures that the plan remains stable even as your team expands.

Aligning your goals with the right plan ensures that NY small business tax credits serve as a permanent foundation for your cash flow. It's about more than just compliance; it's about creating financial serenity for yourself and your team. If you're ready to design a more intentional tax strategy, our team can help you evaluate your tax planning options to find the perfect fit for your firm's future.

Designing Financial Clarity: The Wright CPAs, LLC Advisory Model

Financial clarity is not a fortunate accident. It is the result of deliberate design and a steady, year-round rhythm. Many firms treat their taxes as a seasonal crisis, reacting to deadlines with a sense of urgency that often leads to overlooked opportunities. A fixed-fee advisory model changes this dynamic by removing the friction of hourly billing. It creates a space for deep listening and intentional planning. When the dialogue between an owner and their advisor is continuous, the complex landscape of NY small business tax credits becomes a manageable and predictable terrain.

Moving beyond seasonal preparation allows for a higher level of financial intentionality. We act as the lead architect for your firm's fiscal structure, coordinating directly with retirement plan providers and payroll services to ensure that every available credit is captured. This coordination is vital because the incentives provided by the SECURE 2.0 Act and state mandates require precise timing and documentation. By integrating these elements into a cohesive strategy, we ensure that your business's tax engine is both fully compliant and highly optimized for the 2026 fiscal year.

The Visionary Business Owner

A visionary business owner understands that retirement planning is a bridge to a future exit strategy. It isn't merely about the present year's liability; it's about building a sense of permanence and peace of mind. Consider the example of a Western New York firm that recently redesigned its tax profile. By moving away from a reactive approach and embracing a credit-focused retirement strategy, they were able to lower their annual tax bill while simultaneously securing the owner's eventual transition out of the business. This structural shift provides a foundation of serenity that allows the owner to focus on growth rather than compliance hurdles.

Your Partner in Financial Architecture

Our firm provides the quiet authority needed to navigate the high-stakes environment of New York taxation. For businesses operating in Buffalo, Rochester, and Syracuse, our CFO Services offer a level of guidance that goes far beyond basic bookkeeping. We help you move from contemplation to a finalized 2026 tax strategy, ensuring that every decision is grounded in your specific geographic and cultural context. We value substance over spectacle, focusing on the quality of the intervention rather than the volume of the noise.

The transition to a more resilient financial structure begins with a single, thoughtful conversation. By evaluating your current position and identifying the specific NY small business tax credits available to your firm, we can help you build a more intentional future. Contact us today to begin your structural tax assessment and discover how a refined approach to Tax Planning can improve your daily life and your business's long-term health.

Establishing Your Permanent Financial Foundation

Constructing a resilient business requires a shift from reactive habits to intentional design. The SECURE 2.0 Act and New York mandates provide the raw materials for a stronger fiscal structure. By selecting the right retirement vehicle and utilizing NY small business tax credits, you transform a regulatory requirement into a permanent asset for your firm's cash flow. This isn't merely about compliance; it's about creating a space where your business and your team can flourish with clarity.

True financial serenity comes from having a partner who understands the specific cultural and geographic context of Western New York. Our team of Buffalo-based CPAs specializes in providing the CFO-level guidance and proactive tax strategy required to navigate these complexities. Through our fixed-fee monthly advisory retainers, we offer the steady oversight needed to ensure your financial architecture remains sound and optimized for long-term growth.

Design your proactive tax strategy with Wright CPAs. Let's move from contemplation to a finalized plan that secures your legacy and your peace of mind.

Frequently Asked Questions

What is the SECURE 2.0 tax credit for small business retirement plans?

The SECURE 2.0 tax credit provides a direct reduction of liability for establishing new retirement plans. For firms with 50 or fewer employees, it covers 100% of startup costs up to $5,000 annually for three years. It also includes a five-year credit for employer matching contributions, capped at $1,000 per employee. This framework allows NY small business tax credits to function as a government-subsidized foundation for your team's future.

Does New York State require my small business to offer a retirement plan?

New York requires private-sector employers with 10 or more employees to offer a retirement vehicle if they've been in business for at least two years. The Secure Choice mandate is an automatic enrollment Roth IRA. Businesses that implement a private plan, such as a 401(k) or SIMPLE IRA, are exempt from this state-run requirement. Registration deadlines in 2026 vary by company size, starting as early as March 18 for larger firms.

What is the difference between a tax credit and a tax deduction for retirement?

A tax credit is a dollar-for-dollar reduction in the actual tax you owe. A tax deduction only reduces the amount of your income that is subject to taxation. Credits are more powerful structural assets because they directly lower your final bill. Understanding this distinction is essential for maximizing NY small business tax credits and ensuring your financial architecture is as efficient as possible.

How many employees do I need to qualify for the startup tax credit?

To qualify for the federal startup costs credit, a business must have 100 or fewer employees who received at least $5,000 in compensation in the prior year. The most significant benefits are reserved for the smallest firms. Employers with 50 or fewer employees can claim 100% of their qualified costs. Those with 51 to 100 employees are eligible for a 50% credit on those same startup expenses.

Can I claim the tax credit if I already have an existing retirement plan?

The startup costs credit is reserved for new plans established within the last three years. However, businesses with existing plans can still access specific incentives under SECURE 2.0. If you add an automatic enrollment feature to an existing plan, you may qualify for a $500 annual credit for three years. This incentive rewards the modernization of your current retirement structure without requiring a full redesign.

What are the deadlines for setting up a 401(k) to get 2026 tax benefits?

For a new SIMPLE IRA to be effective for the 2026 tax year, it generally must be established by October 1. Formal plan amendments to reflect SECURE 2.0 provisions must be completed by December 31, 2026. Setting these dates early in your fiscal calendar ensures that your tax strategy remains proactive. It prevents the structural failure of missing out on significant federal and state incentives during the construction phase.

What is the NYS Small Business Subtraction Modification?

The NYS Small Business Subtraction Modification is a structural adjustment that allows eligible entities to subtract a percentage of their net business income from their federal adjusted gross income. Most small businesses can subtract 5%, while farm businesses are eligible for a 15% subtraction. This modification is available to resident individuals, partners, and LLC members whose net business income is less than $250,000.

How do I claim the retirement plan startup costs tax credit on my federal return?

You claim the federal retirement plan startup costs tax credit by filing IRS Form 8881 with your annual tax return. This form calculates the credit for administrative expenses and the new credit for employer contributions. It's a technical exercise that requires precise documentation of your plan's setup costs and matching funds. Proper preparation ensures these credits are captured as permanent improvements to your business's cash flow.